Are you tired of feeling like your finances are spiraling out of control? Worried about overspending and unsure where your money goes each month? Look no further! In this article, we present the ultimate list of budget categories that will help you take control of your financial life.

From essentials like housing and groceries to leisure activities and unexpected expenses, we’ve got you covered. Let’s dive into the world of budgeting and discover how you can achieve your financial goals.

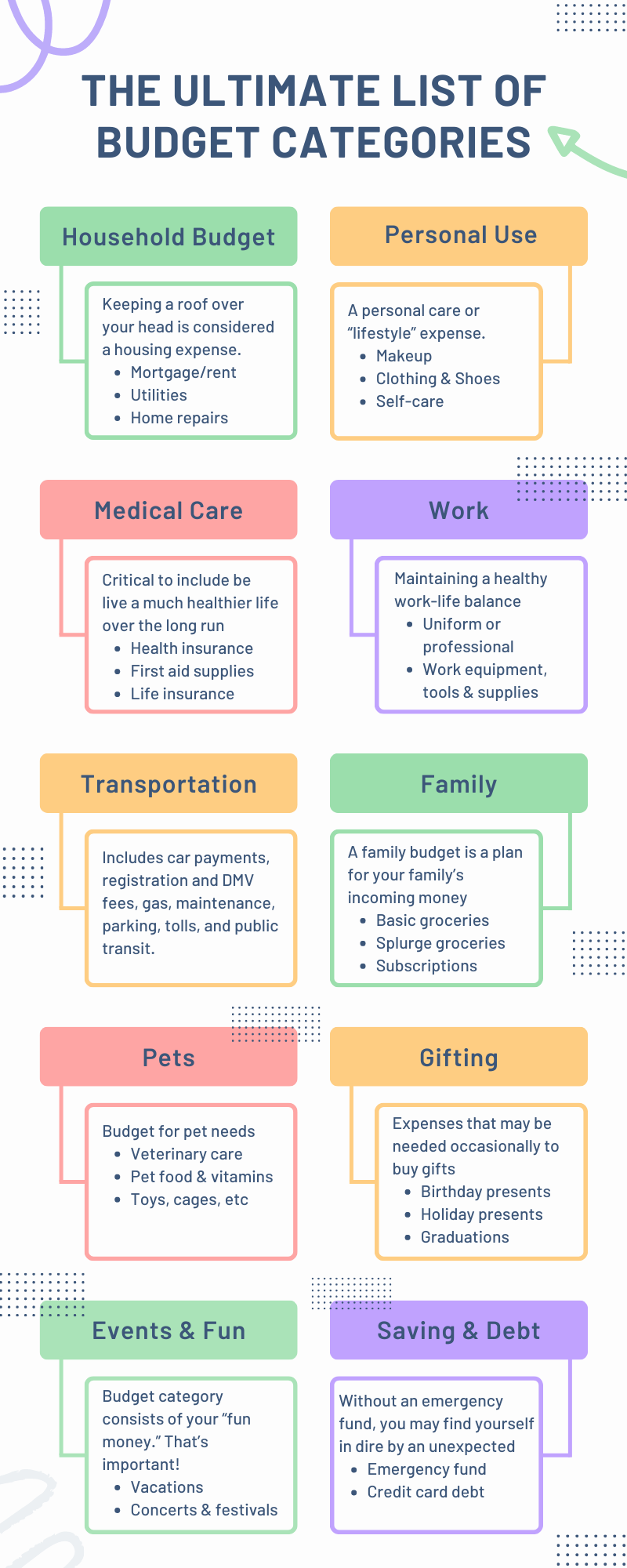

The Ultimate List of BUDGET CATEGORIES

Creating a budget that covers all aspects of your life is the first step towards achieving financial stability. By allocating your income into specific categories, you can track your spending, save more, and make informed financial decisions. Below, we’ve outlined the ultimate list of budget categories to consider incorporating into your budgeting strategy.

We’ve built a personal expense categories list with more than 30 sections, so you can adapt it whether you want a simple plan or go deeper with 100 budget categories that cover every corner of your financial life.

| Category | Description |

|---|---|

| Income (Net) | Track your net income after taxes, including salary, freelance work, or side hustles. |

| Housing | Covers rent/mortgage, property taxes, insurance, utilities, and maintenance. |

| Transportation | Fuel, public transport, car insurance, parking, tolls, and maintenance. |

| Groceries & Household Supplies | Food, beverages, cleaning products, toiletries. |

| Utilities & Connectivity | Electricity, water, heating, internet, mobile. |

| Debt Payments | Loans, EMIs, credit card balances (snowball vs avalanche methods). |

| Savings & Investments | Emergency fund, retirement, brokerage, short-term sinking funds. |

| Insurance Premiums | Health, life, disability, renters, auto, or property insurance. |

| Healthcare | Doctor visits, prescriptions, dental, vision, and medical supplies. |

| Education & Career Growth | Courses, certifications, skill-building. |

| Childcare & Schooling | Daycare, tuition, uniforms, extracurriculars. |

| Elder Care/Family Support | Remittances, medicines, caregiving. |

| Pet Care | Food, vet visits, grooming, insurance. |

| Clothing & Personal Care | Apparel, grooming, skincare, wellness. |

| Subscriptions & Digital | Streaming, software, apps, domains, cloud storage. |

| Home Maintenance & Appliances | Repairs, renovations, replacements, warranties. |

| Home Office | Furniture, peripherals, supplies. |

| Entertainment & Leisure Activities | Movies, hobbies, fitness memberships. |

| Dining Out & Takeout | Eating at restaurants or delivery. |

| Travel & Holidays | Airfare, hotels, visas, trip insurance. |

| Gifts & Festivals | Gifts, birthdays, anniversaries, cultural celebrations. |

| Charitable Giving | Donations to causes and NGOs. |

| Banking & Fees | ATM charges, overdraft, late fees, service charges. |

| Miscellaneous Buffer | Unexpected one-offs not fitting elsewhere. |

This expanded table goes beyond a standard list—almost like a 100 budget categories playbook, helping you avoid hidden leaks and blind spots.

Housing: Finding Financial Stability in Your Shelter

Finding the right balance between a comfortable living space and financial stability is crucial. Housing is often the largest expense in a budget, encompassing various costs that can impact your overall financial health.

Whether you’re renting an apartment or paying off a mortgage, consider these tips to manage your housing expenses effectively:

- Rent vs. Buy: Before making a decision, evaluate whether renting or buying a home is more financially viable for you. Calculate the costs involved in each option, including mortgage payments, property taxes, and maintenance.

- Roommates: If you’re comfortable with it, having a roommate can significantly reduce housing costs, making it easier to allocate funds to other categories.

- Utilities: Be mindful of your energy consumption to reduce utility bills. Consider energy-efficient appliances and practices to lower costs.

- Maintenance: Regular maintenance can prevent costly repairs in the long run. Set aside a portion of your budget for home maintenance and repairs.

- Downsizing: If your current housing situation is stretching your budget, consider downsizing to a smaller space that better suits your financial capabilities.

Transportation: Navigating Your Budget on the Go

Transportation expenses can add up quickly, affecting your overall financial picture. Whether you rely on public transit or own a car, managing transportation costs is essential for maintaining a balanced budget.

Here are some strategies to help you stay on top of your transportation expenses:

- Public Transit: If available, consider using public transportation to save on fuel and parking costs. Monthly passes or discounted fares can provide significant savings.

- Carpooling: Share rides with friends, coworkers, or neighbours to split the costs of commuting.

- Fuel Efficiency: If you own a car, choose a fuel-efficient model and practice fuel-saving habits, such as avoiding unnecessary idling and maintaining proper tire pressure.

- Maintenance: Regular vehicle maintenance can prevent breakdowns and costly repairs. Schedule routine check-ups to catch any issues early on.

- Biking/Walking: For short distances, consider biking or walking to save on transportation costs and promote a healthier lifestyle.

Groceries: Feeding Your Body and Budget

Grocery shopping is a routine expense that can significantly impact your budget over time. By adopting smart shopping habits and meal planning strategies, you can save money while still enjoying delicious and nutritious meals.

Here are some tips to make the most of your grocery budget:

- Meal Planning: Plan your meals for the week ahead and create a shopping list based on your planned recipes. This prevents impulsive purchases and reduces food waste.

- Coupons and Sales: Take advantage of coupons, discounts, and sales to save money on your grocery purchases. Be cautious, however, not to buy items solely because they’re on sale.

- 3. Bulk Buying: Consider buying non-perishable items in bulk to take advantage of lower unit prices. Just be sure to only purchase items you’ll use before they expire.

- Store Brands: Opt for store-brand products instead of name-brand items. Often, the quality is comparable, but the price is lower.

- Avoid Convenience Foods: Pre-packaged convenience foods tend to be more expensive. Opt for whole ingredients and prepare meals from scratch to save money.

Debt Payments: Conquering Debt and Regaining Control

Debt can weigh heavily on your financial well-being, making it challenging to achieve your goals. By prioritizing debt payments and adopting a strategic approach, you can gradually reduce your debt and improve your financial situation.

Consider these strategies to tackle your debt effectively:

- Create a Repayment Plan: List all your debts, including credit cards, loans, and outstanding bills. Prioritize them based on interest rates and start paying off high-interest debts first.

- Snowball Method: Pay off your smallest debts first and then use the money you would have paid toward them to tackle larger debts. This approach builds momentum as you see quick wins.

- Negotiate Interest Rates: Contact your creditors to negotiate lower interest rates, especially if you have a good payment history. Lower rates can significantly reduce the amount of interest you pay over time.

- Consolidation: Consider consolidating your debts into a single loan or credit card with a lower interest rate. This can make managing payments more straightforward.

- Avoid New Debt: While paying off existing debt, avoid accumulating new debt. Use cash or your debit card instead of credit cards to control spending.

Savings: Securing Your Financial Future

Building a robust savings plan is essential for achieving your short-term and long-term financial goals. By consistently setting aside money and making wise investment decisions, you can create a strong financial foundation for yourself.

Here are some steps to kickstart your savings journey:

- Emergency Fund: Start by building an emergency fund that covers three to six months’ worth of living expenses. This fund provides a safety net in case of unexpected financial challenges.

- Automate Savings: Set up automatic transfers from your checking account to a dedicated savings account. Treating savings as a non-negotiable expense ensures consistent contributions.

- Retirement Accounts: Contribute to retirement accounts like a 401(k) or IRA. These accounts offer tax advantages and can help you grow your wealth over time.

- Invest Wisely: Research different investment options and consider diversifying your portfolio to mitigate risk. Consult with a financial advisor if needed.

- Short-Term Goals: Allocate savings for short-term goals like a vacation, buying a car, or making a down payment on a home. Having specific targets keeps you motivated to save.

FAQs (Frequently Asked Questions)

Q: How do I decide on a budget for each category?

A: Start by tracking your current spending for a few months to identify patterns. Then, allocate funds to each category based on your priorities and financial goals.

Q: What if my income varies from month to month?

A: If you have irregular income, consider using a zero-based budgeting approach. Assign every dollar a specific purpose, including saving and covering irregular expenses.

Q: Should I budget for entertainment and leisure activities?

A: Absolutely! Budgeting for leisure activities is essential to maintain a healthy work-life balance and prevent burnout.

Q: Is it okay to adjust my budget as circumstances change?

A: Yes, flexibility is key to successful budgeting. Life is unpredictable, so be prepared to adjust your budget when necessary.

Q: How can I stick to my budget and avoid overspending?

A: Regularly review your budget, track your expenses, and use tools like budgeting apps to stay on track. Avoid impulse purchases and focus on your financial goals.

Q: Is it possible to save money while paying off debt?

A: Yes, it’s possible. Create a balanced plan that allocates funds to both debt repayment and savings. Having an emergency fund can prevent new debt during unexpected situations.

Conclusion: Empower Your Financial Journey

Congratulations! You’ve now explored the ultimate list of budget categories that can transform your financial management approach.

By allocating your income strategically and making informed spending decisions, you’ll be well on your way to achieving your financial goals.

Budgeting isn’t about restriction—it’s about clarity and confidence. With a detailed system (even up to 100 budget categories if needed), you’ll gain financial freedom while still enjoying the things that matter most.